👛 Coinbase - $COIN

Coinbase is operating higher profit margins than Google or Microsoft and growing fast. But the stock is also very volatile and trades at the mercy of the wider crypto market. Let’s weigh up the bull/bear case and decide whether now is a good time to invest.

📱 Product

Coinbase’s main business is a centralised cryptocurrency exchange which makes money by charging a commission on each buy or sell transaction.

The company is also trying to generate revenue from a number of other income streams, these include:

Coinbase One - subscription service for regular users of the platform to trade without fees.

Coinbase Prime - premium service aimed at high net worth individuals and institutional investors, providing security and custody of crypto assets.

Coinbase Cloud - tools and infrastructure for software developers to build blockchain applications.

📈 All Time Stock Price Chart

📊 Key Financials

RoboStox App Snapshot on Monday (February 7th) before market open:

As you can see above, Coinbase is currently trading at a market cap of $50.92 billion, nearly 11 billion more than the London Stock Exchange (also a publicly listed company) which is valued at almost $40bn.

In Q3 2021 (April-June), monthly transacting users were up to 7.4 million compared to Q3 2020 when there were only 2.1 million active users on the platform. But this user metric also declined in Q3 2021 by 1.4 million versus Q2 2021 following a downward trend in the wider crypto market.

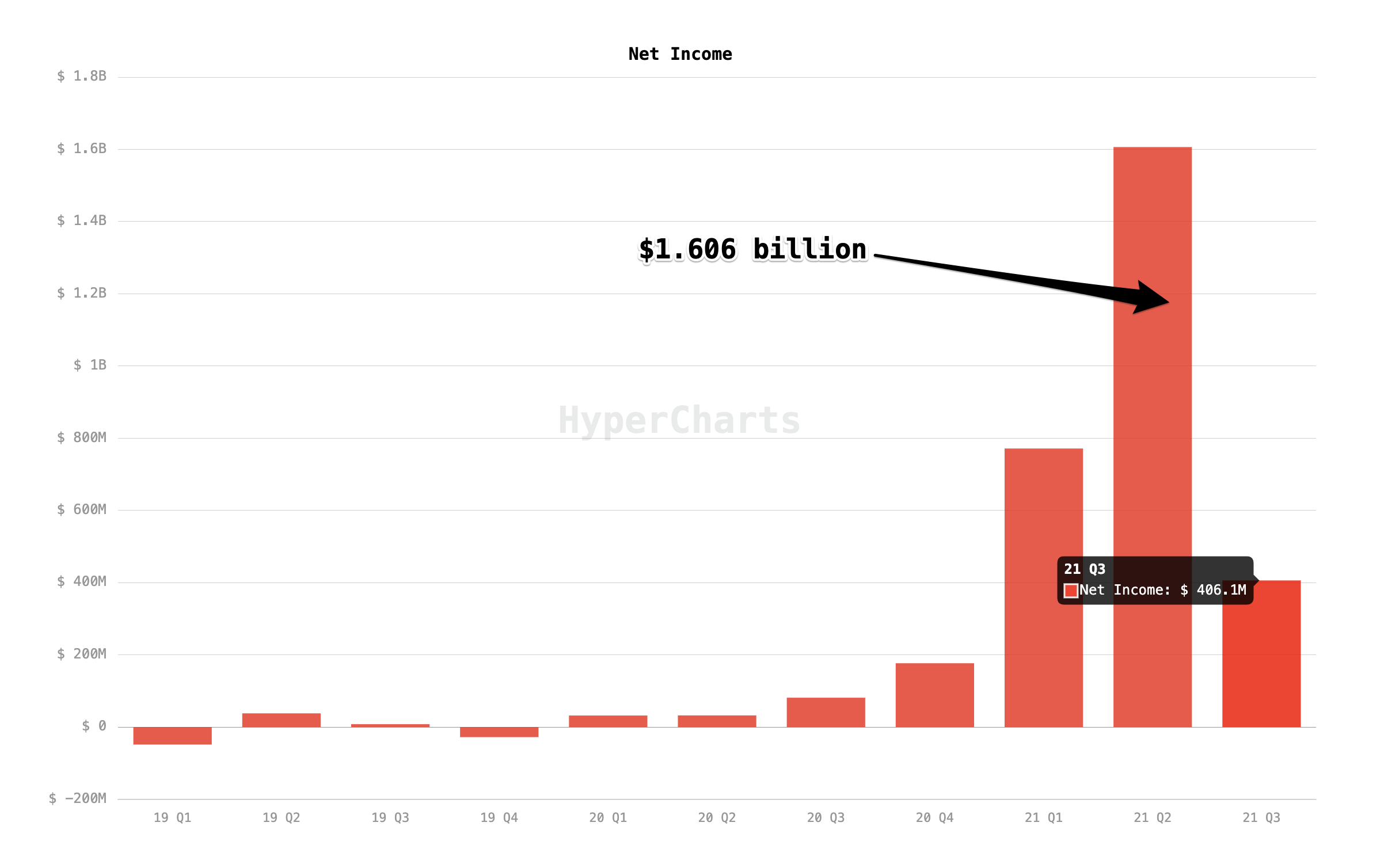

Net Income (total profit after subtracting all expenses) has followed the same pattern as the change in user numbers. The “year-over-year” Q3 figure is up dramatically from $81.3 million in 2020 to $406.1 million in 2021. But when we look at the “quarter-over-quarter” change, this is down big from a high of $1.606 billion in Q2 2021.

Source: Hypercharts Profit Margin: 49.97%. (Google and Microsoft also operate very high margin software businesses and recently reported profit margins of 29.51% and 38.50% respectively).

👨 👩 Leadership

CEO: Brian Armstrong. See last week’s report on Beyond Meat for the rationale on providing information on CEO personal stock sales.

Soon after Coinbase’s IPO on April 14th 2021, Armstrong declared to the SEC (the US regulator) that he owned a total of 1,050,000 shares through a trust he controls.

On the day of the IPO, filings to the SEC show that Armstrong sold 749,999 shares in 3 batches worth a grand total of $291.8 million.

These share sales make-up over 71% of his original holdings. Armstrong’s trust now has 300,358 shares remaining.

🚀 Bull Case

Coinbase stock offers investors wide exposure to the crypto market without having to select specific cryptocurrencies. Many use the analogy of the gold rush: instead of prospecting for gold, buy the company making the “picks and shovels” (the tools) to invest in the crypto market.

Coinbase has one of the best products on the market from an ease-of-use and user experience perspective. They have also built a strong brand which is one of the most trusted in the crypto space. Retail traders are willing to pay slightly higher transaction fees than on other exchanges for this peace of mind.

The company still has a lot of growth potential beyond their core business. Coinbase will launch an NFT marketplace soon which could compete with the biggest market incumbents. OpenSea, the current market leader has just 600,000 users on their platform, while Coinbase has had 1.5 million sign-ups for early access to their NFT product alone. Coinbase’s latest Q3 monthly transacting user figure is 7.4 million. In total there are about 73 million verified users on Coinbase (including those who do not regularly trade).

At 8.6, the price-to-sales ratio for Coinbase stock is much better than Tesla’s at 17.23, and only slight worse than other growth stocks like Netflix and Google which are much more mature businesses. Given Coinbase’s very high growth rates and profit margins it looks under-valued.

🐻 Bear Case

Coinbase is too reliant on transaction fees as its primary revenue source. This makes the stock very sensitive to volatility in the crypto markets. When there is a bull market Coinbase revenue goes up dramatically, but during bearish conditions the reverse is true. The other subscription and institutional-related revenue streams are still unproven as stable forms of income.

Coinbase operates a traditional centralised exchange and as a public company must be fully compliant with US regulations. It will face growing competition from decentralised exchanges which can move faster and offer more innovative products.

CEO Brian Armstrong’s decision to sell a clear majority of his shares (over 71%) on the day of the IPO, should raise some alarm bells about his future commitment to the company. We can contrast this with the CEO of last week’s company Beyond Meat, who sold just 0.34% of his shares.

What did I miss? - These reports are a learning process for me and I’m very open to constructive feedback and suggestions.

What stock or crypto asset should I cover next? You can contact me by email: hellorobostox@gmail.com or feel free to leave your response in the comments below. You can also follow me on Twitter: @daneasterman.

Disclaimer: I am not a financial advisor, none of this report should be taken as financial advice. Instead this should be viewed as starting point to conduct your own research. I do not hold any positions in Coinbase stock at the time of writing.